(A continuation of: “You Need to Know”)

- The association’s wind insurance includes a $20 million sublimit, which may be far below the building’s true insurable value of $118 million.

- The Association was advised that coverage did not meet lender requirements and chose not to increase it due to premium cost.

- This insurance gap directly contributed to a mortgage refinance being declined and could affect future buyers.

- Owners deserve clear disclosure of what coverage is required, carried, and missing to understand their real financial exposure.

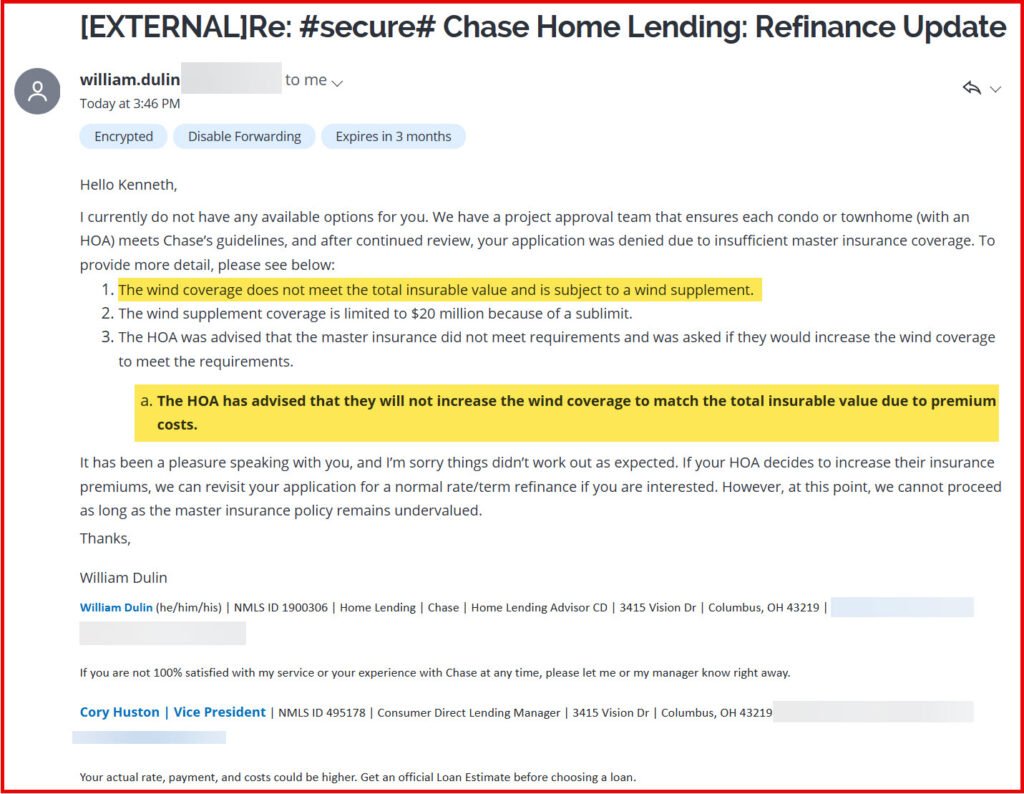

In the previous post, I shared that Chase Bank declined my refinance due to concerns about the association’s master insurance coverage after more than 9 weeks of the association delays in responding to the bank.

When I asked for more detail, the bank provided the following explanation (The full message is posted below):

- The wind coverage does not meet the total insurable value and is subject to a wind supplement.

- The wind supplement coverage is limited to $20 million because of a sublimit.

- The association was advised that the master insurance did not meet lender requirements and was asked whether the wind coverage would be increased.

- “The Association advised that it would not increase the wind coverage to match the total insurable value due to premium costs.“

These statements raise important questions for every owner.

In recent communications, the board has highlighted the savings achieved in our insurance premiums. A significant portion of that reduction, however, resulted from the building becoming fully impact-resistant after the 2023 installation of impact glass in common areas that had no protection. This resulted in a 2024 inspection where for the first time the association was 100% impact resistant.

Those 2023 improvements reduced premiums by roughly 20% on a $2.2 million policy, we now pay around $1.8M. FL insurance law provides we receive an approximate 20% reduction in insurance for being fully impact resistant.

At the same time, we now learn that our wind coverage may not meet lender requirements in a city with a six-month hurricane season.

This can be a potential high liability exposure if we were to get hit by a named storm. If that happened we would probably be assessed to make up the difference in repairs which would be more than the “savings”.

Reminder: Reserves do not cover storm damage.

It should also be noted; condo insurance policies have seen rate relief (Price Reductions) in 2024 and 2025, thanks to law changes and new providers entering the market.

Considering costs of construction in South FL are getting more and more expensive this doesn’t seem intelligent.

For owners who may want to refinance, or sell to buyers who require a mortgage, this is not an abstract concern. Lenders review this information carefully.

It is reasonable for owners to ask:

- Does our current wind coverage adequately protect the building’s total insurable value of $118 million?

- Were owners informed that coverage levels were not being increased due to premium costs?

- How might this affect financing and property values?

These are questions worth discussing with your neighbors and raising at future meetings.

Every owner deserves clarity on this issue.

Original (Part 1) Appears Here

No spam. Just important BK1 News updates.